For the banks in Detroit, Michigan, February 1933 was a loveless month. The industrial state had suffered through the Great Depression, and the slow drain on large banks that began with regional panics in 1930 and expanded throughout the nation in 1931 now increased, with no signs of slowing. Detroit banks liquidated assets and borrowed from the Reconstruction Finance Corporation (RFC), but the Banking Crisis of 1933 was gaining momentum.

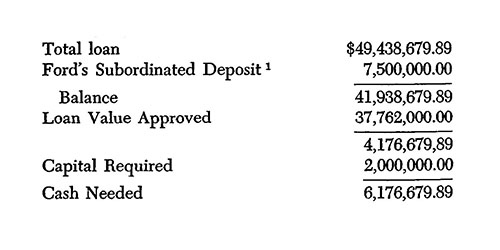

The largest depositor in Detroit banks in 1933 was Henry Ford, head of the Ford Motor Company. Ford held deposit liabilities in the amount of $7,500,000 in the Union Guardian Trust Company. The trust company already held a loan from the RFC but was still in need of funds, so a plan was worked out in which the Guardian Group would pay into the trust company to allow enough assets for it to receive another loan from the RFC that would provide further liquidation for the Guardian National Bank of Commerce. However, the entire plan rested on the basis that the deposit liabilities to the Ford Company be subordinated, a proposal Ford immediately declined.

Guardian Group loan plan, from “Recollections of the Banking Crisis in 1933,” Francis Gloyd Awalt, Business History Review, Autumn 1969.

On February 13, 1933, a meeting arranged by President Herbert Hoover was held in Henry Ford’s office. Secretary of Commerce Roy D. Chapin, Under Secretary of the Treasury Arthur A. Ballantine, Henry Ford, and Edsel Ford (brother of Henry Ford and director of the Union Guardian Group) were present. Ballantine and Chapin explained the situation and the proposal again and urged Ford to subordinate the deposit liabilities held by the Ford Motor Company. This plan, they insisted, was the only chance for the survival of the trust company. Ford again refused, this time advising that if the trust company was not kept open, he would immediately withdraw all Ford deposits from the First National Bank. Ballantine and Chapin stated that this action would not only ensure the end of the trust company, but also cause the First National Bank of Detroit to fail, which would then distress all of the banks in the state of Michigan. This chain of events, they urged, could have a disastrous effect on the nation and, in turn, Ford’s business. Ford stated that if his company were destroyed, he would start a new one and that the general effect of a crash on the people of Detroit would be “everyone would have to get to work a little sooner.”[1]

One day after the meeting with Ford, Governor William Comstock declared an eight-day bank holiday for Michigan, preventing Ford from withdrawing funds from various Detroit banks. The declaration set off a wave of dread across the nation. Other states began to hold their own bank holidays in an attempt to stem bank runs. On March 2, 1933, a series of phone conversations were held between then-President Hoover, Secretary of the Treasury-designate William H. Woodin, and President-elect Roosevelt in an attempt to reach an agreement on a bank holiday that would satisfy both administrations. Calls zipped between New York and Washington during the day and late into the evening, and though proclamation drafts were created, no agreement was reached.

By March 3, the drain on gold reserves had accelerated, with the Federal Reserve Bank of New York losing gold through wire transfers, gold earmarking, and exports and losing more than $150,000,000 in currency. With no policies in place to stem the flow of gold, Federal Reserve Banks were forced to close on March 4.

By the time Roosevelt was inaugurated on March 4, 1933, 48 states had closed banks. On Monday, March 6 at 1:00 am, a mere 36 hours into his presidency, President Roosevelt issued Proclamation 2039.[2] This suspended all banking transactions and immediately began a four-day national banking holiday, allowing Congress time to prepare drafts of the Emergency Banking Act. The Act enabled the 12 Federal Reserve Banks to issue additional currency on good assets so that reopening banks could meet demands, providing deposit insurance for those banks. Roosevelt dedicated his first Fireside Chat to explaining the emergency measures to the American public, instilling hope with the words “Together we can not fail.” On March 13, 1933, most banks reopened to long lines of customers returning their withdrawn cash to their bank accounts. [Image: “Delaware is Last to Act,” New York Times, March 1933.]

An overview of the financial situation from the March 11, 1933, issue of the Commercial and Financial Chronicle outlines the “epoch-making events” in the days after the nationwide bank holiday, asking “how much further the policy of expansion must be carried before there shall be a complete restoration of confidence.” In April, President Roosevelt used his expanded powers over monetary policy to sign an executive order criminalizing the hoarding of “gold coin, gold bullion and gold certificates.” The Emergency Banking Relief Act, a temporary measure, was replaced by the widely-debated[3] Banking Act of 1933 in mid-June. The Act formed the Federal Deposit Insurance Corporation and created the Federal Open Market Committee (FOMC).

The events following the banking crisis in 1933 led to a restoration of trust in the American banking system, created a new framework for monetary policy, and solidified the financial landscape. Before 1933, there was no consistent system for deposit insurance, and the Federal Reserve did not yet have the emergency lending programs of later years.[4] The response of the Federal Reserve during the financial crisis of 2007-2009 is the result of the study of past actions both taken and not taken to avert financial disaster. In a 2009 speech, Chair Ben Bernanke remarked that the policy of the 1930s was “largely passive and political divisions made international economic and financial cooperation difficult,” but noted that the Fed’s “speedy and forceful actions” helped to protect global financial institutions from facing serious risk.

[1] Francis Gloyd Awalt. “Recollections of the Banking Crisis in 1933.” Business History Review, Autumn 1969.

[2] Robert Jabaily. “Bank Holiday of 1933.” Federal Reserve History, November 22, 2013.

[3] Julia Maues. “Banking Act of 1933 (Glass-Steagall).” Federal Reserve History, November 22, 2013.

[4] For an explanation of the Federal Reserve’s monetary policy during the Great Depression, see the following: Dave Wheelock. “Monetary Policy in the Great Depression: What the Fed Did, and Why.” Review, Federal Reserve Bank of St. Louis, March/April 1992.

© 2021, Federal Reserve Bank of St. Louis. The views expressed are those of the author(s) and do not necessarily reflect official positions of the Federal Reserve Bank of St. Louis or the Federal Reserve System.